1028 Livingston Ave West St. Paul MN 55118 Home for Sale

Text 1028 to 952-994-7204 to schedule a showing or get details.

This home is located at 1028 Livingston Ave West St. Paul MN 55118.

Click below to view full photos, pricing, and property details.

If you’re searching for an affordable home in West St. Paul, this one stands out immediately.

1028 Livingston Ave in West St. Paul MN 55118 is priced at just $199,900. That’s rare for a move in ready home with space, updates, and a strong location.

This 1.5 story home offers over 1,200 finished square feet with four bedrooms and one bathroom. You get flexibility. Bedrooms, office, guest space. You decide.

Text 1028 to 952-994-7204 to schedule a showing or get details.

Key features • Newer vinyl windows • Low maintenance aluminum siding • Fenced backyard, perfect for pets or privacy • Deck for relaxing or entertaining • Oversized 2 car garage, hard to find at this price

Located in West St. Paul near Robert Street.

Step outside and you’re close to everything.

You’re within walking distance to local parks, plus a larger park just about a mile away with ball fields, play areas, and open space. This is the kind of location buyers want but struggle to find at this price point.

Location matters. This one delivers.

Living at 1028 Livingston Ave West St. Paul MN puts you just one block off Robert Street. That means quick access to shopping, restaurants, and daily essentials.

• Less than 5 minutes to Highway 494 • Easy access to Crosstown • Under 10 minutes to downtown Saint Paul

If you commute, this saves you time every day.

Why this home makes sense

Homes under $200,000 in this area are extremely limited. Most buyers are competing hard for anything move in ready at this price.

This gives you a chance to: • Own instead of rent • Build equity • Get into the market before prices move higher

You’re not overpaying for luxury. You’re buying smart.

If you are searching for 1028 Livingston Ave West St. Paul MN 55118, this is your opportunity to see it before it’s gone.

Text 1028 to 952-994-7204 to schedule a showing or ask questions.

If you are searching for 1028 Livingston Ave West St. Paul MN 55118, this is your opportunity to see it before it’s gone.

Text 1028 to 952-994-7204 to schedule your showing.

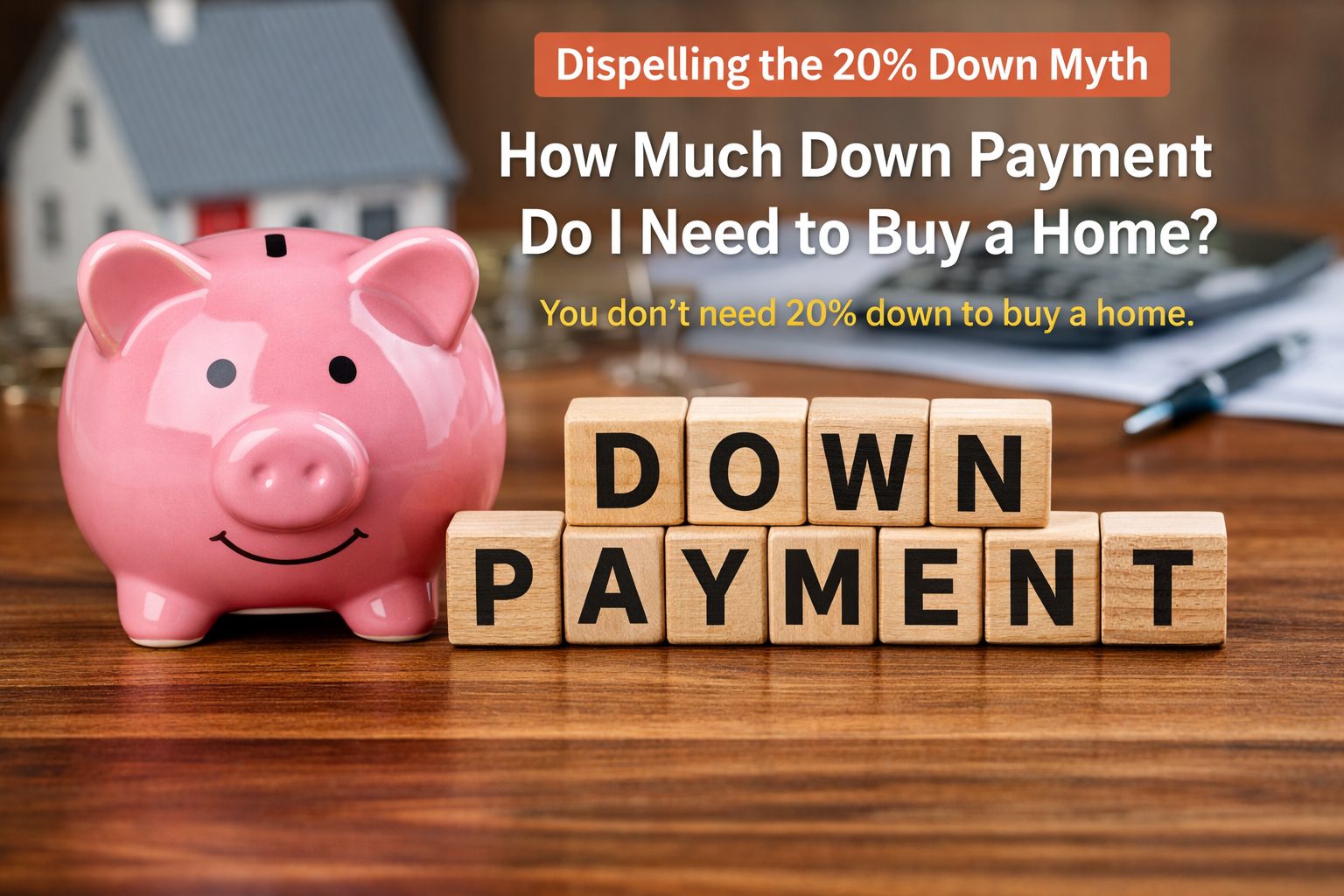

How Much Down Payment Do You Really Need to Buy a Home?

Think you need 20 percent down to buy a home?

That belief is costing you years.

Most buyers wait. They keep renting. They keep saving. And they stay stuck.

You don’t need 20 percent down.

Let’s simplify this.

You can buy a home with as little as 3 percent down using a conventional loan. I’m seeing this work right now in today’s market.

So why does everyone talk about 20 percent?

Because at 20 percent down, you avoid PMI which is private mortgage insurance. It also makes your offer look stronger in competitive situations.

But here is the truth.

Your down payment should match your situation, not some outdated rule.

What I tell my buyers

First, don’t panic.

You do not need 20 percent down to buy a home.

Second, the more you put down, the stronger you look. That matters in multiple offer situations.

Third, if you are not competing with other buyers, your down payment matters a lot less. At that point it becomes about your comfort level, your monthly payment, and what you can realistically afford.

That is the real conversation.

What I am seeing right now

Most buyers are using conventional loans.

Why

Because there are strong 3 percent down options that are getting accepted.

FHA and VA loans still exist, and they can be great tools, but you need to understand how sellers view them.

FHA loans have a reputation. Sellers worry about stricter appraisals and repair requirements.

VA loans offer zero down, which is an incredible benefit if you have served. But in competitive situations, zero down offers tend to get pushed to the bottom because sellers are concerned about timelines and potential hurdles.

It is not personal. It is risk.

What you actually need saved

Here is where most buyers get it wrong.

They focus only on down payment.

You need two buckets of money.

Down payment Closing costs

At a minimum, plan for about:

3 percent down Plus around 3 percent for closing costs

If you can cover both, you are in a strong position.

If you can put more down, even better. It strengthens your offer and lowers your payment.

Real numbers to think about

Here is what 3 percent down looks like at different price points.

On a $300,000 home About $9,000 down

On a $400,000 home About $12,000 down

On a $500,000 home About $15,000 down

Then plan for a similar amount for closing costs.

This is where most buyers have a wake up moment.

The barrier to entry is often lower than they expected.

Stop waiting

Waiting to save 20 percent can cost you years.

Years of rent Years of missed equity Years of watching prices change

There are smart ways to get into a home sooner without overextending yourself.

The key is having the right strategy.

In conclusion

You do not need 20 percent down.

You need a plan.

If you want to know what this looks like for your situation, text or call me at 952-994-7204. I will walk you through your options and help you figure out what makes the most sense for you.

If you have been watching the news lately, scrolling through social media, or just talking to friends and neighbors, you have probably heard some version of this question. Is the housing market about to collapse? Are we headed for another 2008? Should I wait to buy or sell?

I have been selling real estate in the Twin Cities for 23 years. I have seen multiple market cycles, helped clients through the worst of the 2008 crash, and I am watching this market closely every single day. Here is my honest, straight answer — and I am going to give you the context that the clickbait headlines never do.

No. The Housing Market Is Not Going to Crash. Here Is Why.

I want to be clear about something first. There are a lot of people out there with a financial interest in making you scared. Fear drives clicks. Fear drives engagement. Fear sells newsletters and gets people to tune in. But fear is not a real estate strategy and it is not based on what the data actually shows.

That does not mean the market is without challenges. It is not. But a challenging market and a crashing market are two very different things, and understanding that difference could be the most important thing you read this year if you are thinking about buying or selling a home.

What Actually Caused the 2008 Crash — And Why 2026 Is Nothing Like It

To understand why we are not headed for another crash, you have to understand what actually caused the last one. And most people do not.

If you have not seen the film The Big Short, I genuinely recommend it. It does an excellent job explaining in plain language what happened. But here is the short version.

The 2008 crash was driven largely by mortgage-backed securities — banks bundling good loans together with terrible loans and selling the whole package as a AAA investment. They knew what they were doing. The loans inside those packages were built on a foundation that was guaranteed to collapse.

Here is what was happening on the ground during that era. You could walk into a bank with almost no income verification and get approved for a loan. Not just any loan — interest only loans, partial interest loans, and adjustable rate mortgages that started at a payment you could afford and were designed to reset higher in a few years. So instead of buying a $250,000 home they could comfortably afford, people were being talked into $450,000 homes with the same starting monthly payment. When those adjustable rates reset and went up, millions of people suddenly could not afford their mortgage. And because many of them had bought with zero down, they had no equity to fall back on. They were underwater from day one. Foreclosures flooded the market and values collapsed.

That is not what today looks like. Not even close.

What Is Different Right Now

Today’s lending environment is completely different. The loose, anything-goes loan products that fueled 2008 are gone. Borrowers today have to actually qualify for what they are buying.

More importantly, American homeowners right now are sitting on significant equity. That changes everything. If you lose your job or face a hardship and absolutely have to sell, the vast majority of today’s homeowners can do so and walk away with money in their pocket. That was not true for millions of people in 2008 who were underwater from the day they closed.

For homeowners with less than 20 percent equity, private mortgage insurance — PMI — protects the lender. The entire system has been restructured around preventing the kind of catastrophic collapse we saw before.

None of this means the market is easy or that everyone is comfortable. Interest rates have made affordability harder. Uncertainty in the broader economy has made buyers cautious. But caution is not a crash.

What I Am Actually Seeing Right Now in the Twin Cities

Here is where the national conversation completely misses the local reality — and this is what matters most if you are buying or selling in Lakeville, Bloomington, or anywhere in the Twin Cities metro.

The market right now is not one market. It is two very different experiences happening at the same time.

On one hand I am watching certain homes receive ten offers within days of listing. On the other hand I am watching similar homes sit with no activity for weeks. The difference has almost nothing to do with price and everything to do with condition and presentation.

Buyers right now — across every price point — want a home that is move-in ready and completely updated. They will happily pay more for a home that is clean, current, and requires nothing. They will avoid a home that needs work even if it is priced lower. That is the defining characteristic of this market and it is critical information whether you are buying or selling.

In Bloomington the market has been notably active because of the price point. You can get into a home in Bloomington for around $300,000 or more, which opens the door to a much larger pool of first time buyers. That demand is real and consistent.

In Lakeville you are looking at a mid-tier market where $400,000 or more is the starting point for a solid home. But Lakeville commands strong dollar per square foot values because the housing stock is newer and there is significant new construction activity. Buyers in Lakeville are paying for quality and they know it.

Across the Twin Cities broadly the pattern is consistent — whether you are in northeast Minneapolis, Richfield, Rosemount, or Burnsville. Move-in ready homes with strong presentations are getting competed for aggressively. Homes that need updating, have weak photos, or are overpriced are sitting regardless of neighborhood. And if you do not have a strong offer and a solid down payment, competing in the active segments of this market is genuinely difficult right now.

So What Should You Actually Do?

If you are sitting on the sidelines waiting for a crash that is not coming, you are likely watching your opportunity get more expensive every month. Values in the Twin Cities are not collapsing. They are adjusting in some segments and holding or growing in others.

If you are a homeowner worried about your equity, the data says you are in a far stronger position than the headlines suggest. Your equity is real and it is protecting you in a way that 2008 homeowners simply did not have.

If you are thinking about selling, the most important thing you can do right now is not wait for a better market. It is to position your home correctly — price it right, prepare it properly, and market it in a way that reaches the buyers who are actively looking. That is exactly where the difference between sitting and selling is made in this market.

Have Questions About What This Market Means for You?

Whether you are buying or selling in Lakeville, Bloomington, or anywhere in the Twin Cities, I am happy to give you a straight, honest read on what your specific situation looks like right now.

No pressure. No pitch. Just real information from someone who has been doing this for 23 years and has seen this market from every angle.

Call or text Tom Sommers directly: 952-994-7204

Tom Sommers | Coldwell Banker Realty | Serving Lakeville, Bloomington, and the Twin Cities Metro Area

If you are buying or selling a home in Lakeville, Bloomington, or anywhere in the Twin Cities metro area, the home inspection is one of the most important steps in the entire process. I have been doing this for 23 years and I can tell you that what happens during and after an inspection can make or break a deal — and in some cases, save a buyer from a very expensive mistake.

Let me walk you through exactly what to expect, and share a few things I have learned along the way that most agents will never tell you.

What Is a Home Inspection?

A home inspection is a visual examination of a property’s condition performed by a licensed inspector. It is not a pass or fail test. It is an honest look at the current state of the home — what is working, what is not, and what could become a problem down the road.

In Minnesota, home inspectors are licensed by the state and must follow established standards of practice. A thorough inspector will walk you through their findings in plain language and give you a written report with photos, usually within 24 hours.

Who Orders It and When?

In most cases the buyer orders and pays for the inspection. It typically happens within a few days of an accepted purchase agreement, during what is called the inspection contingency period. In the Twin Cities market that window is usually five to ten days depending on how the contract is written.

Sellers can also choose to order a pre-listing inspection before putting their home on the market. This can be a smart move because it lets you find and fix issues before buyers discover them — which puts you in a much stronger negotiating position.

What Does an Inspector Actually Look At?

A licensed inspector examines the home from top to bottom. Here is what is typically covered:

Roof — Shingles, flashing, gutters, and visible signs of wear or damage.

Foundation and Structure — Cracks, settling, moisture intrusion, and overall structural integrity.

Electrical System — Panel condition, wiring, outlets, and basic safety.

Plumbing — Water pressure, visible pipes, water heater condition, and signs of leaks.

Heating and Cooling — Furnace and air conditioner age, condition, and basic function.

Insulation and Ventilation — Attic insulation and ventilation, which matter a great deal in Minnesota winters.

Windows and Doors — Operation, sealing, and signs of moisture between panes.

Basement and Crawl Space — Moisture, mold, structural concerns, and sump pump condition.

Garage — Door operation, fire separation, electrical, and structure.

Interior — Ceilings, walls, floors, stairs, and visible signs of water damage or deferred maintenance.

Plan on two to four hours depending on the size of the home. Buyers — show up for at least the last hour so the inspector can walk you through the findings in person. This is not optional in my opinion. More on that in a moment.

A Story That Has Stayed With Me

Early in my career I had buyers fall in love with a three level split — clean, well cared for, showed beautifully. Everything looked great on the surface. But the inspector noticed something that most people would have completely missed.

The backyard had been filled in improperly and the grading around the foundation was wrong. According to the inspector the home should have been built up two more courses to account for the slope of the yard. Because it wasn’t, water was being directed toward the foundation instead of away from it. There was already minor water intrusion in the basement — very slight, easy to dismiss — but the inspector was clear: without major regrading, possibly bringing in a bobcat to reshape the yard, this problem was going to get worse over time.

My buyers had no idea. The sellers may not have fully understood it either. But because we had an inspector who truly understood the building process, my clients were able to make an informed decision about whether this was a home they still wanted to buy and under what terms.

That is exactly what a good inspector is supposed to do. And that is exactly why who you hire matters enormously.

The Biggest Mistake I See Buyers Make

Uncle Bob.

I say this with respect because I know Uncle Bob means well. Maybe he spent 20 years in construction. Maybe he built his own garage. But here is the reality — a licensed home inspector who is active in this market is doing 500 or more inspections per year. That is a level of pattern recognition and experience that is very hard to match.

Uncle Bob has seen a lot of homes. A great inspector has seen thousands, and they know exactly what to look for in Minnesota homes specifically — frost heave, ice damming, inadequate ventilation, improper grading, aging mechanicals. Do not skip a professional inspection to save a few hundred dollars on a transaction that involves hundreds of thousands.

How I Help My Clients Choose the Right Inspector

This is something I do differently than most agents and I think it matters.

When I am working with a buyer I give them a list of five or more credible, licensed inspectors in the Minneapolis Saint Paul metro area. Along with that list I give them a set of questions to ask when they call. Then I tell them to actually make the calls.

Call each one. Have a real conversation. Ask them about their experience with the type of home you are buying — older construction, new builds, split levels, condos. Ask how they deliver their report. Ask if they encourage buyers to be present. Pay attention to how they communicate and whether they make you feel informed or overwhelmed.

The inspector you hire should be someone you feel genuinely comfortable with — because when that report comes back you are going to have questions, and you need someone who will give you straight answers.

It takes an hour of your time to make those calls. It is absolutely worth it.

What Happens After the Inspection?

The inspector delivers a written report, usually within 24 hours, documenting everything they found with photos. These reports can range from a few pages to 50 or more depending on the home’s age and condition.

Here is where buyers and sellers both tend to get tripped up. Every inspection report has a list of items. Every single one — including brand new construction. The goal is not a perfect report. The goal is understanding what is significant versus what is routine maintenance.

There are generally three categories of findings:

Safety issues — The most important. Faulty electrical panels, carbon monoxide concerns, compromised foundations. These need to be addressed, period.

Functional issues — Things that are not working as they should. A broken window, a failing water heater, an HVAC system at the end of its life.

Maintenance items — Normal wear and tear. Caulking, dirty filters, minor grading issues. These are informational and typically not negotiation items.

As your agent my job is to help you read that report clearly and figure out what to do next.

Can You Negotiate After an Inspection?

Yes. In Minnesota buyers have the right to negotiate repairs, a price reduction, or a seller credit based on inspection findings — as long as it falls within the inspection contingency period.

Sellers are not required to fix everything. But significant findings open the door to real conversation. Knowing what to ask for, how to ask for it, and when to stand firm versus when to walk away is something that comes from doing this for a long time. I have been navigating inspection negotiations in this market for 23 years and my job is to protect your interests on both sides of the table.

What a Home Inspection Is NOT

It is not an appraisal. It does not determine market value.

It is not a code compliance inspection. Inspectors flag safety concerns but they do not certify that a home meets current building code.

It is also not a guarantee. Inspectors can only report on what is visible and accessible on the day of the inspection.

If the report surfaces something specific — signs of past water intrusion, an aging roof, anything structural — it may be worth bringing in a specialist for a second opinion before you make your final decision. I will always tell you when I think that is the right move.

Have Questions About the Inspection Process?

Whether you are buying or selling in Lakeville, Bloomington, or anywhere in the Twin Cities South Metro, I am happy to walk you through what to expect and how to handle whatever comes up.

Text or call Tom Sommers directly: 952-994-7204

No pressure. No obligation. Just honest advice from someone who has been doing this for a long time and genuinely wants to help you make the right move.

Tom Sommers | Coldwell Banker Realty | Serving Lakeville, Bloomington, and the Twin Cities Metro Area

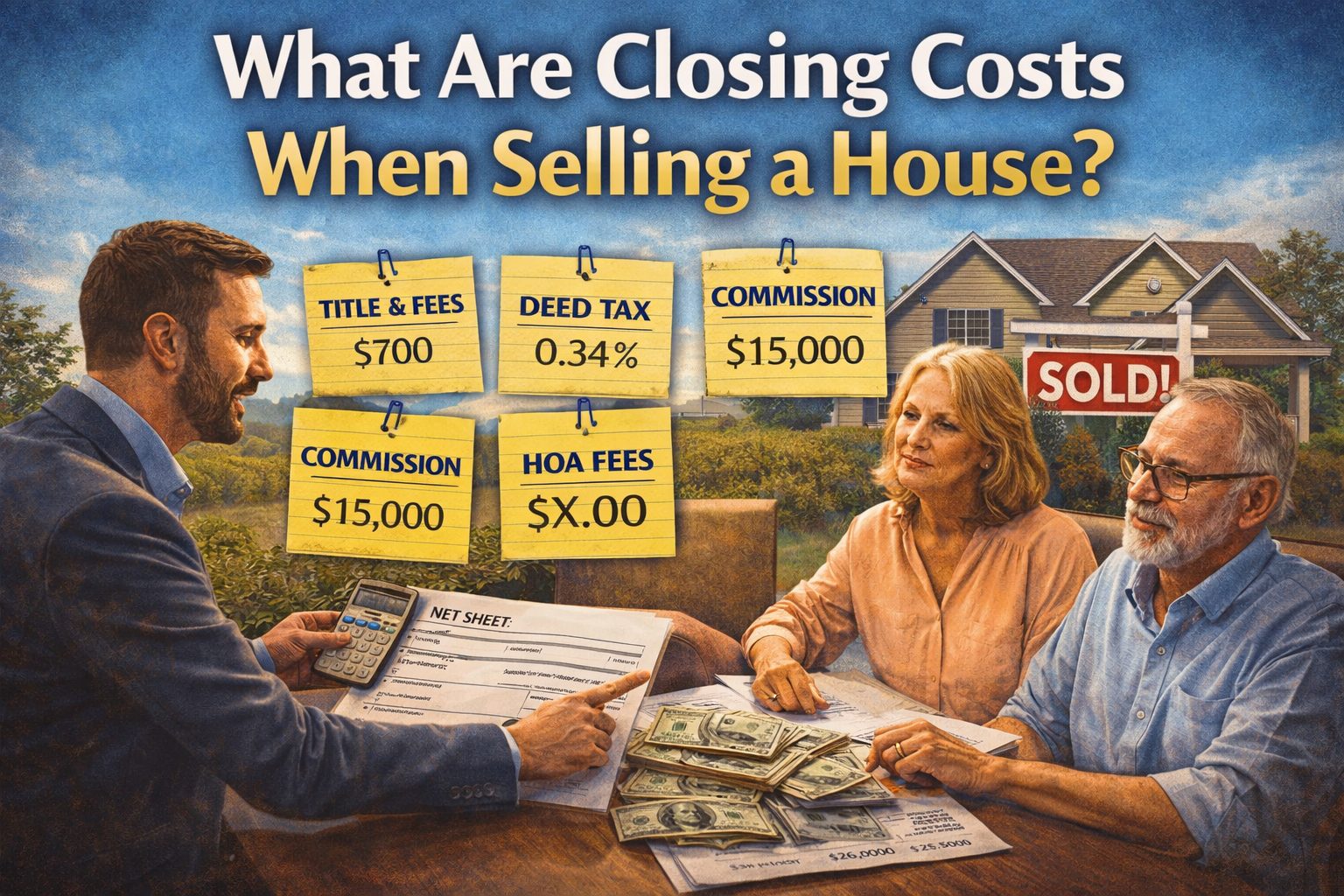

If you are selling your home, you want one clear number. What will you walk away with at closing?

Seller closing costs are lower than buyer costs. But you still need to know what is included.

Here are the typical seller closing costs:

Title and closing fee around $700

County fees around $92

State deed tax about 0.34 percent of the sale price

HOA related fees if you are in a townhome or association

These costs are straightforward and easy to estimate.

Now let’s talk about commission.

Commission is not technically a closing cost. It is part of the real estate transaction. It is also one of the largest expenses and it directly affects your bottom line.

Here is what matters:

Commission is negotiable

It is agreed upon between you and your agent

It is fully disclosed upfront

It is included in your net sheet

When I meet with sellers, I include commission in the net sheet so you see your true bottom line. There is no guesswork.

The net sheet shows:

Sale price

Mortgage payoff

Closing costs

Commission

Estimated proceeds

In most cases, I am within about $1,000 of the final number.

You also need to be aware of title work.

Sometimes a lien or judgment shows up. This could be a credit card or past debt. The title company finds this early so we can resolve it before closing. In many cases, we can negotiate these liens and still move forward with the sale.

Property taxes and insurance can adjust your final number depending on timing. Those are the only variables.

The key is simple.

When everything is laid out upfront, there are no surprises. You know exactly where you stand before your home even hits the market.

If you are thinking about selling and want a detailed net sheet that shows exactly what you will walk away with, call or text 952-994-7204.

Should You Buy a Home Now or Wait for Interest Rates to Drop?

If you are thinking about buying a home, you are asking one question. Should you buy now or wait for rates to drop?

Here is what is happening right now.

Interest rates are around 5.75 percent. Down from nearly 8 percent a year and a half ago. That sounds like a reason to wait. Most buyers think the same way.

That is where the problem starts.

When rates drop, more buyers enter the market. Inventory is still low. That creates competition fast.

What that looks like in real time:

More showings

More offers

More bidding wars

Homes under $300,000 are getting hit the hardest. I saw one this week with 22 offers in 48 hours on a home in Bloomington. You are not negotiating in that situation. You are competing.

Many buyers believe waiting saves money. In most cases, it costs more.

When rates drop:

Prices go up

Buyers push offers higher

Homes sell $25,000 to $50,000 or more over asking

I am already seeing this happen.

I recently helped a buyer purchase a home in Lakeville just under $600,000. Based on current activity, similar homes in that neighborhood will likely list closer to $625,000 soon. That buyer moved early and avoided the next wave of competition.

Here are the biggest mistakes buyers are making right now:

Asking sellers to pay closing costs in a competitive market

Looking at homes without being pre approved

Waiting until after they find a home to talk to a lender

If you are not ready, you miss the opportunity. Homes are selling too fast.

You need:

A loan officer

A clear plan

Full pre approval before you start

Market differences matter.

Lakeville:

Typically $400,000 and up

New construction influences pricing

Buyers comparing new vs existing homes

Bloomington:

Roughly $250,000 to $400,000

Strong demand for starter homes

Faster sales and more multiple offers

Different price points. Same pressure. Limited inventory and strong demand.

Here is the bottom line.

You know what is in front of you today. You know the rates. You know the inventory.

You do not know what happens next.

If rates drop, more buyers enter. Prices rise. Competition increases. You risk paying more later.

If you are serious about buying and want a clear plan based on today’s market, call or text 952-994-7204.

What Increases Home Value the Most? (Top Upgrades That Actually Sell Homes for More in 2026)

If you’re thinking about selling your home, you’ve probably asked yourself: “What upgrades actually increase my home’s value the most?”

Here’s the truth most sellers don’t hear: 👉 You don’t need to spend $50,000 on renovations to get top dollar. 👉 But you do need to make the right updates — not just the ones you personally like.

After working with real sellers and seeing what buyers respond to right now, here are the upgrades that consistently make the biggest impact.

🏡 1. Clean, Decluttered, and “Model Home” Ready (The Foundation)

Before spending a dollar on upgrades, this matters most:

Deep cleaning

Decluttering every room

Removing personal items

Creating a “model home” feel

Buyers don’t just buy houses — they buy how a home feels.

🍽️ 2. Updated Kitchens (Without Full Renovation)

Kitchens sell homes — but that doesn’t mean a full remodel.

What works:

New stainless steel appliances

Painted cabinets (white or neutral tones)

Updated hardware

Clean, bright finishes

👉 Buyers want modern, clean, and move-in ready, not necessarily luxury.

🛁 3. Updated Bathrooms (Simple > Expensive)

You don’t need a spa remodel.

Focus on:

New fixtures

Fresh caulking and grout

Updated lighting

Clean, neutral finishes

Small updates here go a long way in buyer perception.

🪵 4. Flooring That Feels New and Modern

Flooring is one of the biggest visual upgrades.

Top performers:

Wide-plank hardwood flooring

Updated neutral carpet (with a quality pad)

💡 Pro tip: You can save money on carpet — just invest in a better pad for a higher-end feel.

🎨 5. Neutral Paint = MASSIVE ROI

This is one of the highest-return upgrades you can make.

What buyers want:

Light, neutral tones

Consistency throughout the home

One of the most effective colors I recommend:

👉 Accessible Beige (Benjamin Moore)

What to avoid:

Gold tones

Burnt orange

Pastels

Bold personal color choices

🚨 Sellers often make the mistake of painting for themselves instead of the market.

🌳 6. Curb Appeal That Gets Buyers in the Door

First impressions matter more than ever.

Focus on:

Fresh exterior paint (if needed)

Clean landscaping

Mulch, edging, and trimming

A clean, welcoming entry

If buyers don’t like the outside, they may never walk in.

⚠️ What Sellers Get Wrong (And It Costs Them Money)

The biggest mistake I see:

👉 Updating based on personal taste instead of what buyers want

Examples:

Choosing outdated colors

Installing cheap-looking materials

Keeping honey oak woodwork because “it’s still in good shape”

Reality:

👉 Most buyers today prefer white, bright, and modern finishes

📉 Real Example: Small Changes = Big Results

I recently worked with a seller who didn’t want to paint their home.

The home sat with strong showing activity

No offers

After making simple changes:

Repainted from gold/orange tones → neutral beige

Replaced carpet with a clean, modern look

👉 The result? The home sold within a week (with only a small price adjustment).

💰 The Truth About Increasing Home Value

You don’t need to overspend.

👉 You need to:

Focus on high-impact updates

Keep everything neutral

Make the home feel move-in ready

And most importantly:

👉 Price your home correctly based on its condition

🚀 Final Takeaway

You can dramatically increase your home’s value with relatively small, strategic updates.

But if your goal is to:

Sell faster

Attract stronger offers

Maximize your profit

👉 You need to prepare your home the right way before listing.

📞 Thinking About Selling?

If you’re curious:

What updates are actually worth it for your home

What you should (and shouldn’t) spend money on

How to maximize your sale price

👉 Let’s talk. 952-994-7204

I’ll walk through your home and give you a clear, no-pressure strategy to help you put the most money in your pocket.

This is one of the biggest misconceptions I see with home buyers, especially first-time buyers. Most people walk in thinking one of two things: either they need 20% down, or they believe they can buy a home with nothing down. In reality, most buyers fall somewhere in between.

Over the years, I’ve worked with many first-time buyers who assumed they couldn’t afford to purchase a home because they didn’t have 20% saved. The moment they find out that options like FHA loans require as little as 3.5% down, or that some conventional loans allow as little as 3% down, it completely changes their outlook. That realization alone has helped many people move forward with buying when they otherwise wouldn’t have.

The biggest mistake I see isn’t just the down payment—it’s the lack of understanding around the full picture. Closing costs often catch buyers off guard. While there are ways to structure an offer where the seller helps cover those costs, many buyers don’t fully understand how that works going in, which creates unnecessary stress.

One thing I always emphasize is that the down payment decision shouldn’t be made in a vacuum. I rely on experienced loan officers to walk buyers through their specific options, because guidelines and programs change constantly. What I encourage my clients to do is simple: ask their lender to show them real numbers at different price points. For example, what does a monthly payment look like at $300,000 versus $325,000 or $350,000? Once you see those numbers, it becomes much easier to decide what feels comfortable—including how much to put down.

There’s also a difference depending on the market. In areas like Bloomington, where many homes are more affordable and attract first-time buyers, I commonly see lower down payments around 3.5%. In Lakeville, where prices are often higher, buyers tend to put anywhere from 5% to 20% down, especially if they’re moving up from another home.

The truth is, you do not need 20% down to buy a home. Putting 20% down can help you avoid private mortgage insurance (PMI), but that doesn’t mean it’s always the right move for everyone. In fact, PMI has become much more affordable in recent years, making lower down payment options even more practical.

At the end of the day, the right down payment is the one that puts you in a comfortable financial position—not just to buy the home, but to enjoy it after you move in.

If you have questions about what your options might look like, text HOMES to 952-994-7204 and I’ll help you get pointed in the right direction.

How Long Does It Take to Sell a House in Today’s Market?

One of the most common questions homeowners ask is, “How long will it take to sell my house?”

The honest answer is that it depends on several factors, and the real estate market can shift quickly. In my experience, I’ve seen conditions change dramatically in as little as two weeks depending on interest rates, buyer demand, and available inventory.

Looking back over the last six months gives us some perspective. The fall of 2025 through the end of the year was relatively slow in many markets. A major reason was mortgage interest rates. Rates had been elevated for quite some time, and while they have been gradually declining, many buyers were waiting for them to drop further before entering the market.

As we move into the spring of 2026, interest rates for a 30-year fixed mortgage are hovering around roughly 5.75%, though the exact rate depends on factors such as your credit score, debt-to-income ratio, and loan program. A good loan officer can walk buyers through those details and help determine the best options available.

While interest rates and market conditions certainly influence how quickly a home sells, the factor I see making the biggest difference is the condition of the property.

Location will always matter, but two homes in the same neighborhood can have dramatically different results depending on how well the home is prepared for sale.

The first part of condition is presentation. A clean, decluttered home immediately gives buyers confidence in what they’re seeing. When I work with sellers, I always recommend removing excess items from countertops, tables, and shelves. Magnets on the refrigerator, piles of paperwork, and toys scattered throughout the home can make spaces appear smaller than they really are.

My goal when preparing a home for sale is to make it look as close to a model home as possible. Think of the property as a blank canvas that allows buyers to picture their own furniture and lifestyle in the space.

Small maintenance items are equally important. Things like repairing dripping faucets, replacing broken light switches, fixing doors that don’t close properly, and ensuring all lights work properly can make a big difference in how buyers perceive the home.

The second aspect of condition involves updates and improvements. This doesn’t necessarily mean spending $100,000 on a complete remodel. Often, simple upgrades such as fresh paint, updated lighting fixtures, replacing dated trim or doors, and modernizing hardware can dramatically improve how a home shows.

Buyers today tend to gravitate toward homes that feel fresh and move-in ready. At the same time, homes that sit on the market for months often become overlooked by buyers who are constantly watching for the newest listings.

I frequently see homes that have been on the market for six months or longer, even though there’s nothing fundamentally wrong with them. In many cases, the issue simply comes down to presentation or small improvements that could have been addressed before listing.

There’s an old saying in real estate: you never get a second chance to make a first impression. Buyers today are looking at many properties online, and it only takes a few seconds for them to decide whether they want to see a home in person or move on to the next listing.

That’s why preparing your home properly before it hits the market is so important.

Rather than guessing what improvements might help, the best step is to bring in an experienced agent early in the process. I always recommend having a conversation before any work begins so we can walk through the home together and identify the improvements that will provide the greatest return.

More often than not, the biggest difference comes from decluttering, cleaning, and addressing small repairs rather than spending large amounts of money on major renovations.

If you’re considering selling your home and want to know how quickly it could sell in today’s market, I’d be happy to take a look and walk you through your options.

Text HOMES to 952-994-7204 and I’ll help you create a strategy to prepare your home and position it for the best possible result.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link